In the heart of the Pacific, Tuvalu, a nation with approximately twelve thousand residents, is experiencing the early stages of digital financial services. While traditional banking remains limited, the emergence of loan applications, or "loan apps," offers a new avenue for accessing credit. These services provide a rapid way to borrow small amounts, often directly from a smartphone. As a financial expert, my aim is to equip you with the knowledge needed to navigate this evolving landscape safely and effectively.

Current Digital Lending Market Overview in Tuvalu

Tuvalu's digital credit market is still in its infancy, shaped by unique local conditions and regional oversight. As of late 2025, approximately five thousand four hundred adults own smartphones, representing about forty-five percent of the adult population. Mobile data coverage extends to around eighty-five percent of inhabited islands, laying a foundation for digital services, albeit with ongoing challenges.

Access to traditional bank loans is rare for many Tuvaluans, with a significant seventy percent of credit demand being met through informal channels or by regional micro-lenders. This highlights the critical role digital lending could play in financial inclusion.

The regulatory framework for digital lenders in Tuvalu is robust, despite the nation lacking its own central bank. Consumer credit licensing and supervision are managed under a shared arrangement with the Reserve Bank of Fiji, following the 2018 Pacific Financial Inclusion Framework. All digital lenders operating in Tuvalu must register as regional licensed entities, adhere to anti-money-laundering checks, and, crucially, cap their annual percentage rate (APR) at sixty percent. This cap is a vital consumer protection measure.

Typical loan requests range from one hundred to five hundred Australian dollars, with repayment periods, or tenors, usually lasting between seven and thirty days. Approximately one thousand two hundred Tuvaluans are estimated to be active digital borrowers each month, showing a growing, though modest, uptake of these services.

Technology Adoption and Mobile Money Integration

While smartphone penetration and mobile data coverage are growing, they still present constraints compared to more developed markets. Digital lenders in Tuvalu have adapted by using lightweight applications and integrating various forms of data for underwriting. This includes leveraging mobile identification, telecommunications data, bank transaction scraping, and even social network analysis. Loan disbursements often occur through mobile wallets or direct bank transfers, with some providers also utilizing face-to-face agents for a hybrid approach, acknowledging the local context.

Major Loan App Companies and Platforms in Tuvalu

Several regional and international micro-lenders have entered the Tuvaluan market, offering services tailored to the small population. Here are profiles of the most prominent verified loan applications:

-

PacificCash:

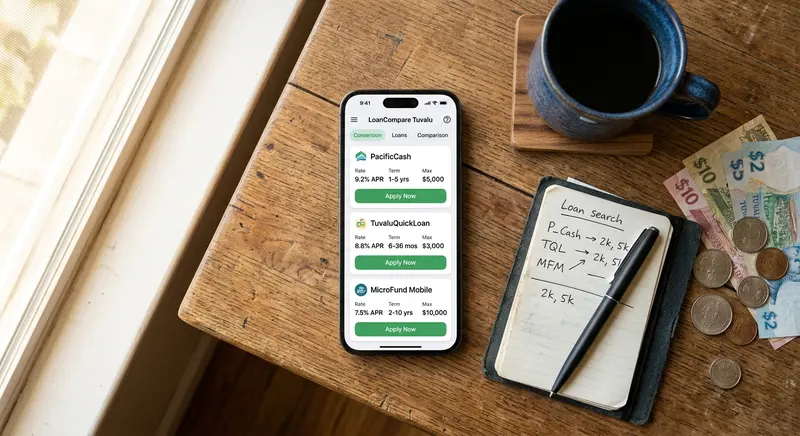

Headquartered in Suva, Fiji, PacificCash offers loans from fifty to five hundred Australian dollars with an APR typically ranging from twenty-eight to forty-eight percent. Borrowers incur a five Australian dollar origination fee and a late fee of ten Australian dollars per day. Onboarding involves mobile identification and a selfie for identity verification. PacificCash uses proprietary scoring alongside telecommunications data for underwriting. It is a licensed regional lender with a strong brand and a Play Store rating of 4.2 out of 5, known for simple onboarding, though occasional app crashes occur. Its main strength lies in its established regional presence, but its product range is somewhat limited.

-

TuvaluQuickLoan:

Based in Brisbane, Australia, TuvaluQuickLoan provides loans between one hundred and three hundred Australian dollars, with an APR from thirty-five to sixty percent. Fees include an eight Australian dollar processing fee and a five percent rollover fee. User onboarding requires email and SMS one-time passwords, with underwriting based on bank transaction scraping. While registered in Fiji, it is currently under an unresolved anti-money-laundering review. It boasts rapid approval and has a Play Store rating of 3.8 out of 5, but its helpdesk support has received poor feedback, and regulatory scrutiny is a concern.

-

MicroFund Mobile:

Operating from Manila, Philippines, MicroFund Mobile offers smaller loans, ranging from twenty to two hundred Australian dollars, with a lower APR of twenty-four to forty percent. Notably, it charges no origination fee, only a seven percent penalty for late payments. Onboarding uses Facebook login and email for identity verification, and underwriting relies on social network analysis. It is a licensed lender with no enforcement actions and a high Play Store rating of 4.5 out of 5, praised for its clean user interface, though payment disbursements can be slow. Its low APR is a significant advantage, offset by the slower payment process.

-

OceanCredit:

Headquartered in Auckland, New Zealand, OceanCredit provides loans from one hundred fifty to six hundred Australian dollars, with an APR between forty and fifty-five percent. It has a ten Australian dollar origination fee and a fifteen Australian dollar per day late fee. Onboarding requires a New Zealand driver's license and a selfie, with underwriting based on credit bureau and telecommunications data. OceanCredit is a licensed lender with an intuitive user experience and a Play Store rating of 4.0 out of 5, despite limited language options. Its strengths include a broad loan range, but its fees are relatively high.

-

DigiKuai:

From Singapore, DigiKuai offers loans from fifty to four hundred Australian dollars, with an APR ranging from thirty to forty-five percent. It charges a three percent origination fee and a four percent rollover fee. Onboarding involves national identification and facial liveness detection, with an artificial intelligence risk engine for underwriting. Licensed in Fiji and accredited in Singapore, it has a fast user experience and a Play Store rating of 4.3 out of 5, though its scoring methods can be opaque. DigiKuai is tech-driven but faces challenges with transparency.

-

IslandFunds:

Based in Nadi, Fiji, IslandFunds provides loans from eighty to three hundred fifty Australian dollars, with an APR between twenty-five and fifty percent. It charges a seven Australian dollar origination fee and a penalty of ten percent of the due amount. Onboarding uses a unique hybrid approach, combining face-to-face agents with app-based verification. Underwriting is a blend of agent assessment and algorithms. It is licensed, though it received a minor warning in 2023 regarding its advertising. With a Play Store rating of 4.1 out of 5, it offers personalized service but its app can be clunky, and stability issues have been noted.

-

SwiftLoan Tuvalu:

With its headquarters in Honolulu, USA, SwiftLoan Tuvalu offers loans from one hundred to five hundred Australian dollars, at an APR of forty-five to sixty percent. Fees include a twelve Australian dollar origination fee and a five percent early repayment fee. Onboarding requires a passport and address proof, and underwriting involves bank API integration and a psychometric test. It is a licensed lender with no enforcement actions. With a Play Store rating of 3.9 out of 5, it is known for rigorous, detailed workflows, but its Know Your Customer (KYC) process can be slow, leading to slower credit decisions.

Comparative Overview of Key Digital Lenders

To provide a clear picture, here is a summary of the verified providers based on their APR, maximum loan amounts, disbursement methods, and user ratings:

- PacificCash: APR range 28-48%, maximum loan 500 AUD, uses mobile wallet, Play Store rating 4.2/5.

- TuvaluQuickLoan: APR range 35-60%, maximum loan 300 AUD, uses bank transfer, Play Store rating 3.8/5.

- MicroFund Mobile: APR range 24-40%, maximum loan 200 AUD, uses e-wallet, Play Store rating 4.5/5.

- OceanCredit: APR range 40-55%, maximum loan 600 AUD, uses bank transfer, Play Store rating 4.0/5.

- DigiKuai: APR range 30-45%, maximum loan 400 AUD, uses mobile wallet, Play Store rating 4.3/5.

- IslandFunds: APR range 25-50%, maximum loan 350 AUD, uses agent cash payout, Play Store rating 4.1/5.

- SwiftLoan Tuvalu: APR range 45-60%, maximum loan 500 AUD, uses bank transfer, Play Store rating 3.9/5.

Interest Rates, Loan Amounts, and Terms

The digital lending landscape in Tuvalu is characterized by specific ranges for interest rates, loan sizes, and repayment terms. As observed across the active platforms, Annual Percentage Rates (APRs) typically fall between twenty-four and sixty percent. These rates reflect the higher operational costs, inherent risks associated with lending in remote areas, and the costs of regulatory compliance.

Loan amounts are generally small, starting from as low as twenty Australian dollars from providers like MicroFund Mobile, and going up to six hundred Australian dollars with OceanCredit. The most common range for loans is between one hundred and five hundred Australian dollars. Repayment terms are typically short, often spanning from seven to thirty days, which is common for micro-lending designed for immediate, short-term financial needs.

Beyond the principal amount and APR, borrowers must be aware of various fees. These can include origination fees (e.g., five Australian dollars for PacificCash, ten Australian dollars for OceanCredit), processing fees (e.g., eight Australian dollars for TuvaluQuickLoan), and late fees (which can be substantial, such as ten Australian dollars per day for PacificCash or fifteen Australian dollars per day for OceanCredit). Rollover fees, charged when a loan is extended, are also common (e.g., five percent for TuvaluQuickLoan, four percent for DigiKuai), and some apps even charge an early repayment fee (e.g., five percent for SwiftLoan Tuvalu). It is crucial for consumers to understand all these charges before committing to a loan, as they can significantly increase the total cost of borrowing.

Regulatory Environment and Consumer Protection

The regulatory structure for digital lending in Tuvalu, overseen by the Reserve Bank of Fiji, is designed to provide a layer of consumer protection. The sixty percent APR cap is a cornerstone of this framework, aiming to prevent excessively high interest charges. All digital lenders must undergo a licensing process and comply with anti-money-laundering regulations, which adds a degree of legitimacy to the verified operators.

However, despite these protections, consumers face several risks:

- High APRs and Compounding Fees: While capped, the APRs are still considerably high compared to traditional banking. The combination of high interest and various fees, especially rollover fees, can quickly lead to a debt spiral if loans are not repaid on time.

- Data Privacy Concerns: Oversight on data privacy can be thin. Some apps may have opaque data-use policies, meaning personal information could be shared or used in ways not fully understood by the borrower.

- Over-borrowing: The ease of access to short-tenor loans can tempt individuals to borrow repeatedly or beyond their capacity to repay, leading to chronic debt.

- Unlicensed Providers: The market may contain unverified or unregistered entities operating outside the regulatory framework. These providers pose a significant risk of predatory practices, exorbitant fees, and even fraud, with no legal recourse for consumers. It is vital to avoid such platforms.

- Technical Barriers: Issues like app crashes, slow disbursements, or customer service unresponsiveness can lead to missed payments or delayed access to critical funds, creating further financial stress.

Market Trends and Future Outlook

Tuvalu's digital lending market is expected to experience slow but steady growth. Key trends include a gradual increase in smartphone penetration and improved mobile data infrastructure across the islands. This will likely encourage more regional players to consider entering the market, potentially leading to increased competition among licensed entities.

Future opportunities exist in the expansion of mobile money services, which could streamline loan disbursements and repayments. The development of robust digital identity solutions could also simplify the onboarding process for borrowers while enhancing security. Government-led initiatives for financial inclusion will be crucial in supporting this growth, alongside efforts to improve digital literacy among the population.

However, challenges persist. The small market size of Tuvalu, coupled with its geographical remoteness, makes it less attractive for large-scale investment. Regulatory complexities, particularly with regional oversight, require consistent monitoring and adaptation. The continued reliance on informal credit channels suggests a need for greater awareness and trust in formal digital alternatives.

Overall, the future outlook points towards a maturing market with increasing emphasis on consumer protection and financial education. As technology becomes more integrated into daily life, digital lending will play an increasingly important role, but vigilance and informed decision-making by consumers will remain paramount.

Practical Advice for Consumers

As digital lending continues to grow in Tuvalu, it is essential for you, the consumer, to approach these services with caution and an informed mindset. Here are five practical recommendations to ensure safer borrowing:

- Verify Licensing: Always ensure that any loan application you consider using is officially registered and licensed under the Reserve Bank of Fiji's regional framework. Using unlicensed providers exposes you to significant risks, including predatory lending and fraud, with no regulatory body to turn to for help.

- Compare APRs and Fees: Do not just look at the loan amount. Thoroughly compare the Annual Percentage Rate (APR) and all associated fees across different providers. Some apps, like MicroFund Mobile, may offer lower APRs but might have slower disbursement times. Weigh the total cost against your immediate needs and tolerance for delays. Understand origination fees, processing fees, late fees, and rollover charges before you commit.

- Read Privacy Policies: Your personal data is valuable. Take the time to read and understand the privacy policy of any loan application. Avoid providers with vague or opaque data-sharing clauses. Be clear about how your information, including your mobile identification, telecommunications data, or bank transactions, will be used and protected.

- Opt for Bank Transfers: Whenever possible, choose loan applications that disburse funds directly to your bank account or a verifiable mobile wallet. This reduces the risk of lost funds or disputes compared to informal cash agents, offering a more secure and traceable transaction record.

- Build Credit History: Start with small loan amounts that you are confident you can repay on time. Consistently making timely repayments on reputable apps, such as PacificCash, can help you build a positive credit history. This can potentially improve your credit scoring over time, which might lead to access to larger loan amounts or more favorable interest rates in the future.

Remember, borrowing responsibly means only taking what you genuinely need and can comfortably repay within the agreed timeframe. Always understand the full terms and conditions before you agree to a loan. By following these recommendations, you can harness the convenience of digital lending while protecting your financial well-being.